After more than 40 years of operation, DTVE is closing its doors and our website will no longer be updated daily. Thank you for all of your support.

COVID-19 hits satellite sector, but video decline reflects HTS development

Fixed Satellite Services (FSS) operators have been hit significantly by the COVID-19 pandemic, particularly those involved in the mobility business, while an ongoing decline in demand for video capacity is set to continue, according to a report by satellite research outfit Euroconsult.

Euroconsult’s FSS Operators: Benchmarks & Performance Review reported increased competition and strong impact from COVID-19 in the US$10.8 billion FSS market – a figure that excludes vertically-integrated operators that provide, for example, direct-to-consumer services as well as satellite capacity.

Euroconsult’s FSS Operators: Benchmarks & Performance Review reported increased competition and strong impact from COVID-19 in the US$10.8 billion FSS market – a figure that excludes vertically-integrated operators that provide, for example, direct-to-consumer services as well as satellite capacity.

Most publicly listed operators reporting on a quarterly basis have reported lower revenues for Q3 2020 than for the prior year, and after the first three quarters of the year, these companies have reported revenues down an average 4% year-over-year, according to Euroconsult.

The industry’s downward trend in revenues is driven by growing High Throughput Satellite (HTS) competition, which has led to significantly lower capacity pricing in recent years, according to the research company’s report. Video demand began to decrease in 2019, before the pandemic, and is set to continue in 2020, which also impacts FSS operators.

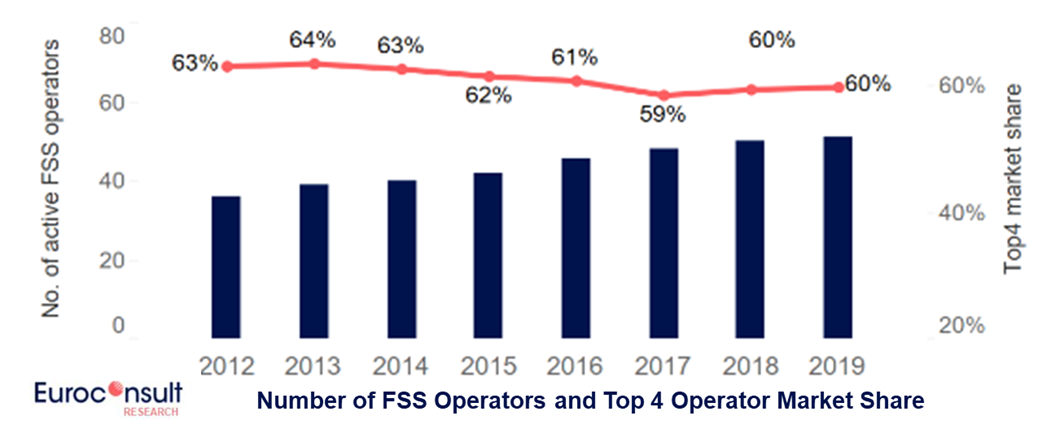

In 2019, the top five FSS operators represented 64% of the industry revenues and 20 operators had revenue of more than US$100 million. Demand for satellite capacity increased by 18% to reach 1,425Gbps. Eight new FSS operators emerged between 2017 and 2020 and six more are expected to enter the market between 2021 to the mid-2020s, according to the research outfit.

According to Euroconsult, close to half of the FSS operators increased the number of regular transponders leased throughout 2019 and service revenues have also grown.

The overall situation is pushing a growing number of FSS operators to look for other sources of revenues. Euroconsult observed that some operators are turning to vertical integration to differentiate, as highlighted by the recent acquisitions of Bigblu Broadband by Eutelsat and Gogo by Intelsat.

“Operators with exposure to the mobility market have suffered the most from the Covid-19 pandemic,” said Dimitri Buchs, Senior Consultant at Euroconsult, and author of the report.

“However, revenue declines appear to be decreasing as the year progresses, maybe a sign of what to expect in 2021.”